Why Everyone Needs Life Insurance

I know. I couldn’t have picked a more exciting topic to talk about, right? Although we don’t like to think about it, death comes to us all…

I know. I couldn’t have picked a more exciting topic to talk about, right? Although we don’t like to think about it, death comes to us all. For those of you reading this who feel like it won’t come to you, I’m sorry to rip off that Band-Aid for you. Even Superman will have his day.

But life insurance is something I would argue everyone in the world needs to have. I know that seems ridiculous to some, but I believe every person in every situation should have some life insurance. Now, within that, we make choices. For example, if someone is older and/or unhealthy, it may not make mathematical sense to purchase life insurance. However, in terms of pure need, I argue everyone needs it.

Let’s break it down. Some people just absolutely need it. For others, it’s a little bit more difficult to make an argument, and those people may not see the benefit, but I still believe they and their family could absolutely benefit from life insurance.

The Obvious Reasons

Can’t Afford Funeral Expenses

Most people think of life insurance for funeral expenses. Sadly, huge portions of the population couldn’t come up with a few thousand dollars to pay for a funeral. The average cost of a funeral varies, but generally a funeral can run from slightly less than $10,000 up to $15,000. “Oh I’ll just be cremated. Throw me in a ditch. I don’t care.” Well, that’s a cute deflection but that will still be at least $3,000, sir.

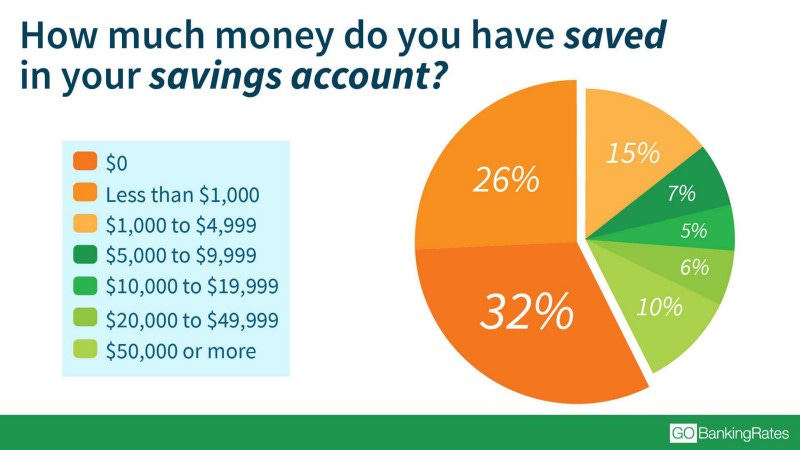

So how many people could actually come up with the money? Statistics vary, but somewhere between 33 percent and 58 percent of Americans could not come up with $2,000. A 2019 Yahoo! Finance study shows only 21% of Americans do have $10,000 to their name.

So naturally, what is the solution? Either sell off your lawnmowers and fine china or simply look at what it would take to get some life insurance.

To Cover Other Debt

We just went over the fact that most don’t have $10,000 lying around. How many people have the amount to cover their mortgage? The average American mortgage of late is well over $200,000. Very few people have that kind of money. Most rely on their current income to pay their bills. What happens if they’re in a car wreck? What if they get cancer?

Also included in these type of debts would be business loans, car loans, student debt (usually forgiven at death but not always), personal lines of credit, credit cards, medical bills, and whatever other debts we may collect in life.

Loss of Income

As agents and advisors, we have these conversations on a daily basis. This particular one has the widest range of responses. To some, it’s incredibly obvious that income is a huge factor in purchasing life insurance. Others are mind-boggled that losing income is that big of a deal.

A typical question I ask in an appointment is, “What is your greatest asset?” What do you think the answer usually is? You guessed it. Usually, people say, “My house” or maybe if they’re a business owner, “My business” or if they’re a property owner or just simply a little more well-to-do, “my investments”.

Would you believe it if I said those answers are usually incorrect? Anyone who makes any type of income most likely has more future income than any possible asset they currently have. If someone just makes $40,000 a year, is 40 years old, and plans on retiring at 65, how much money will they make from now until the time they retire?

$1 million!

If you make more, it’s even more. If you make $100k or more, your future income amounts to several million dollars. If you just make $20,000 a year, 20 years of that is still $400,000! That’s nothing to sneeze at. If you don’t protect your future income with life insurance, you are leaving anyone that relies on you in a HUGE hole.

Pay for Education

Yet another reason to get life insurance is to pay for your kids. As a father of young girls, trust me! Kids cost money. They’re not cheap, and you spend a ton of money on your kids each year, even if you’re not taking vacations and burning through your savings on frivolous trips. Imagine if something happens to you and/or the other adult in your household. That income is lost, and you’re also now flying solo and will likely lose income because of having to play mother and father for however many kids you have.

On top of that, once they grow up, there’s the need for the college or career fund. These needs can be incredibly substantial. Think of all of the single mothers and fathers out there that struggle to make ends meet. Why? They were either left alone by the other parent, or the other parent passed away. It’s a disaster for the family if they’re not prepared.

The Not so Obvious

Covering Young Children

This story stands out to me. My father is an agent. He had to communicate this to my mom, but sometimes these things need to be said. He said, “What if Matthew is hit by a car or he’s out on his bike and wrecks or something else happens?” My mom’s response? “I’d be devastated and wouldn’t want to come out for a year.” Exactly! If you think it’s not a big deal to get coverage on kids, think again.

This is not to get rich off of a child’s death. This is to have enough to survive the aftermath. Put yourself in that spot. Be honest! One of your kids gets killed. What would your response be? You’re probably not going to run back in to work the next day and earn a promotion with your incredible focus and drive. Any sane person would want to crawl in a hole and die if that ever happened. So yes, it would cover a funeral (which you would probably spend more on as a tribute), but it would/could also cover lost income while you and/or your spouse learn to tie your own shoes again.

Also, an important side note: If you get coverage on kids now, if they have health conditions later, they already have some insurance in place. Children are generally insurable, but sometimes conditions can develop that prevent a young adult from being able to easily get life insurance.

Outliving the Nest Egg

This happens quite often in retirement. Mamaw and Papaw are sitting on their retirement, but they live longer than they think they will. Maybe they shouldn’t have gone on so many trips early in retirement. Maybe they should have calculated five extra years. Maybe there was absolutely nothing they could have done.

With modern medicine, people are living longer, and consequently outliving their assets. If your retirement covers you until you’re 83, what happens when you hit 84? If you have enough savings to cover you and your spouse until age 69, what about afterwards? Just because everybody in your family died at a certain point does not mean we can plan on the same timeline.

Having a small life insurance from fairly early on guarantees even if you run out, you’re going to have enough to take care of business.

A good rule of thumb: If you don’t have $1,000,000 behind you, you could possibly run out.

That is not a joke. I’ve seen it happen. More on that in the next section.

Long Term Care Recuperation

Does anyone dream of getting stuck in a nursing home? Does anyone dream of having someone else bathe them? Of course not. But it happens, doesn’t it? How many stories have you heard of where the family just can’t do it anymore, no matter what they pledged to each other? It happens. If someone is going to pay cash for full service long term care, the average American in long term care can fully expect to pay more than $200 per day. Some areas, you can pretty much bank on over $300/day. If you want something nice, you can go up from there.

So one thing you can do is purchase life insurance with long term care protection, but another idea is to purchase life insurance enough to recoup the inevitable expenses of getting older with declining health.

Large Estate/Legacy Planning

Lastly, there are people with significant assets that will never have to worry about running out of money. However, if you’re one of those people, you’ve worked extremely hard to get where you are, and surely, if you can, you’re going to try to leave something to family, to an organization, to make an impact, something. Well, one of the greatest obstacles to legacy and estate planning is tax burden. When we invest in life insurance, that money is invested tax free, and when it pays out, we do not pay a dime on that money. If you have an estate of $20 million and you have a $20 million life insurance policy that pays out, you will pay massive taxes on the $20 million in your estate. However, that full $20 million comes to your beneficiaries in full. It cannot be touched by Uncle Sam.

So Who is Left Out?

It’s one thing to not believe in life insurance, to not feel like you can afford a certain rate to get your ideal amount, or to make a decision not to carry it because you most likely won’t need it. I understand that not everyone has the same level of need. Not everyone is going to feel the need for life insurance. But it’s still there whether you perceive it or not.

Besides the people that just don’t care if they leave their family at risk, everyone should consider life insurance (or some alternative) as an option.

I have seen regret on every level of the spectrum. To the poorest widow with no money wishing she had something, to the richest mogul complaining about his taxes, every person could use life insurance to their advantage. Why not look into it?

I firmly believe everyone should look at their life insurance and consider either why they don’t have it or if they need more.